The United States is experiencing long-term decline in its associational life and that is impacting giving and most forms of charitable interaction. There should be policy reform so that less of the charitable giving by Americans is subject to taxation. “Doing so would be more consistent with the principle that people should not be taxed on money they give away,” according to the authors of “Reforming the Charitable Deduction.”

The report touches on current tax policy and options to boost giving, such as an above-the-line deduction for giving or a credit worth a percentage of the value of a taxpayer’s total giving. Released this week, it discusses trends in charitable giving and their implications for civil society. It also delves into what the authors consider to be issued caused by the current charitable deduction and proposes reforms to make tax policy fairer toward charitable giving and civil society.

The report is from the Social Capital Project, an undertaking by the Joint Economic Committee (JEC) – Republicans. The JEC is a bipartisan economic committee involving both the U.S. House of Representatives and the Senate. This report was sponsored by the Republican members of the JEC.

“Our institutions of civil society have weakened and withered, and our relationships have become more circumscribed,” according to the authors. “Reversing these trends and rebuilding civil society will require capitalizing on the strengths of America’s associational life to address its weaknesses.” That means, according to the authors, reform of charitable giving tax policy.

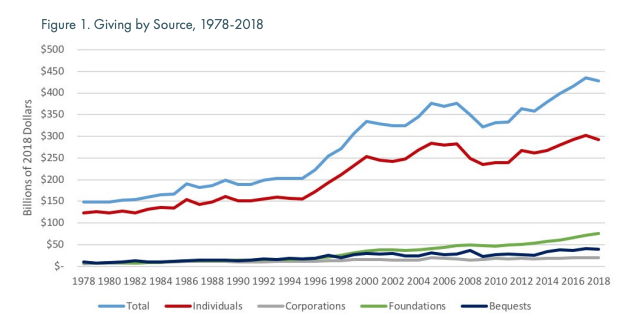

With many of the largest reported donations going to educational institutions, the authors hypothesized on the impact of the shift to major gifts. “The very causes being supported are likely to change as higher-income Americans increasingly drive individual giving. That worsens the problem of crowd-out of civil society because lower-income and middle-class Americans are more likely to direct their giving toward service and assistance to the poor — an area where government crowd-out has been especially severe,” according to the report.

Americans give to charity for many reasons but those decisions include the cost of giving. “When weighing the effects of changes to the charitable deduction, policymakers must consider how reforms might increase new donations, affect tax revenues, and implicate taxpayer compliance and administrative costs,” according to report. A possible change to the rules to entice giving might be setting a floor, giving the deduction at a certain level or as a percentage of the donor’s adjusted gross income (AGI).

A tax provision with a floor, while producing more giving than the current deduction, would have a smaller effect on giving and reduce revenue by less than one without a floor, according to the authors. Based on various reports, the authors suggested that an above the-line deduction with a floor of $500 for single filers and $1,000 for married filers would increase giving by $19.1 billion in 2018 and reduce revenue by $14.6 billion; a 25 percent credit with a floor of $500 for single filers and $1,000 for married filers would increase giving by $20 billion in 2018 and reduce revenue by $15.4 billion. In both cases, only with a floor would the increase in giving exceed the reduction in revenue.

The JEC was created when Congress passed the Employment Act of 1946. Under this act, Congress established two advisory panels: the President’s Council of Economic Advisers (CEA) and the Joint Economic Committee. Their primary tasks are to review economic conditions and to recommend improvements in economic policy. Chairmanship of the committee alternates between the Senate and House every Congress. The current chair is Sen. Mike Lee (R-Utah).

To view the full 18-page report, go here