The unprecedented bull market of the past decade looks great for returns of college endowments and foundations but it will be increasingly harder to continue to earn those types of gains.

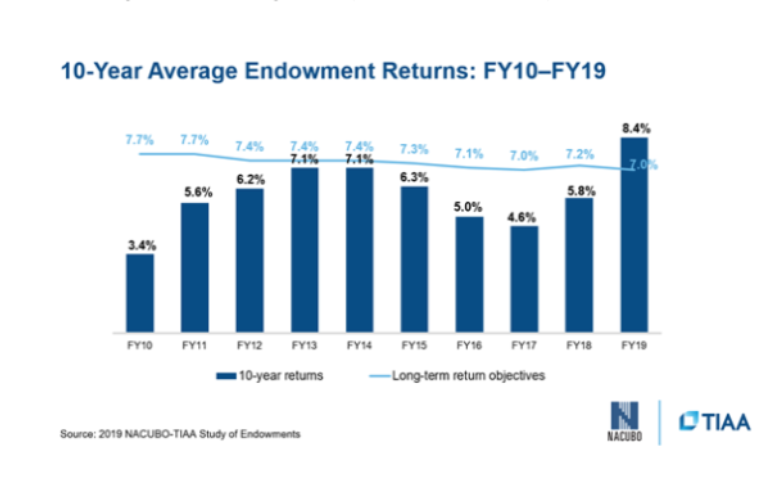

The latest 10-year returns reached 8.4 percent for Fiscal Year 2019, while short-term returns were closer to 5 percent, according to the 2019 NACUBO-TIAA Study of Endowments (NTSE) released today. The average one-year return was 5.3 percent for Fiscal Year 2019, ending in June, following returns of 8.2 percent in 2018 and 12.2 percent in 2017. By comparison, the Dow Jones Industrial Average (DJIA) returned 22 percent for calendar year 2019, after dropping 5.8 percent in 2018, and up 25 percent in 2017.

The 774 U.S. colleges, university, and affiliated foundations in the NTSE represented $630 billion in total endowment assets as of June 30, 2019. The median endowment was approximately $144.4 million, and 39 percent of study participants had endowments of $101 million or less. The National Association of College and University Business Officers (NACUBO) represents chief administrative and financial officers at more than 1,900 colleges and universities in the United States. TIAA is a provider of financial services in the academic, research, medical, cultural and government fields.

Overall, average net annualized returns have been between 5 and 9 percent:

- 5.3 percent, one-year;

- 8.7 percent, three-year;

- 5.2 percent, five-year; and,

- 8.4 percent, 10-year.

Average one-year returns last year by endowment size ranged from 4.9 percent to 5.9 percent while three-year returns ranged from 8.3 percent to 9.6 percent; five-year returns from 4.9 percent to 6.1 percent, and 10-year returns from 7.7 percent to 9 percent.

Average performance across different size foundations ranged from 4.9 percent to 5.9 percent, with highest returns occurring at the largest institutions. Larger institutions outperformed others based on strong results of their large exposures to buyout and venture capital investments.

“Endowment asset allocations and returns varied across different size endowment cohorts. Considering larger endowments generally have greater access to certain asset classes, such as private equity and venture capital, which were some of the highest performing asset classes in FY19, they again outperformed their smaller cohorts,” Kevin O’Leary, chief executive officer of TIAA Endowment and Philanthropic Services, said.

Average 10-year returns reflect the removal of Fiscal Year 2009, the first after the Great Recession, dropping -18.7 percent one-year return from the calculation. The average return of 8.4 percent during the past 10 years is a result of the “very strong recovery period” after a 19-percent drawdown in 2009, according to Dimitri Stathopoulos, head of U.S. institutional at Nuveen, a TIAA company. Even in an extended recovery period, down years are expected, such as in 2012 (-0.3 percent) and 2016 (-1.9 percent), but they’ve been very small. The most recent 10-year average, Stathopolous said, “is not reflective of a full capital market cycle.”

Three-quarters of institutions increased spending from their endowments to support students and faculty, with an average increase of more than $2 million, due in part to strong 10-year returns. Participating institutions put 49 percent of endowment spending dollars to student financial aid, 17 percent to academic programs, 11 percent to faculty, and 7 percent to campus facilities.

Investment oversight committees are shifting their market expectations and long-term endowment return objectives are trending down, from a high of 7.7 percent in FY10 to 7 percent in FY19. Average effective spending rates among respondents was up slightly, from 4.4 percent in FY18 to 4.5 percent in FY19.

Expectations and budgeting for expected returns is moving lower since the financial crisis. “Moving forward, it’s going to be harder and harder to continue to get those types of returns, considering where the economy is, where we are in the cycle of this recovery,” O’Leary said.

The 10-year return is most important, O’Leary said, but encouraged examination of even longer horizons, like the 15- and 20-year returns, which were 6.7 and 6.2 percent, respectively. The 10-year “includes just one segment of this overall market cycle, and it’s been a longer recovery,” he said. “Focus on the future but be very diligent in how you manage liquidity of the portfolio, how to satisfy in-year demands of our institutions,” O’Leary said.

The one-year benchmark is important for the assessment of management itself but long-term returns are “extraordinarily important for the folks handling budgeting and planning,” said Liz Clark, vice president, policy and research, for NACUBO.

Had someone invested in just the S&P 500 over the last 10 years, they would have looked really smart, O’Leary said, but the amount of risk taken would have been massive. “Portfolios are there to balance what we have — global equity, fixed income, alternatives — it’s all a balance to create consistent returns that will help us match what we need to spend in a year, also safeguard future years spending policies, intergenerational equity,” he said.