The total value of assets maintained within 403(b) retirement plans was $1.1 trillion in 2020, up from $851 billion in 2010, according to a new study. These plans — retirement savings options for public sector and tax-exempt sector-employees — realized this increased value despite hardship withdrawals made during the coronavirus pandemic, study authors reported.

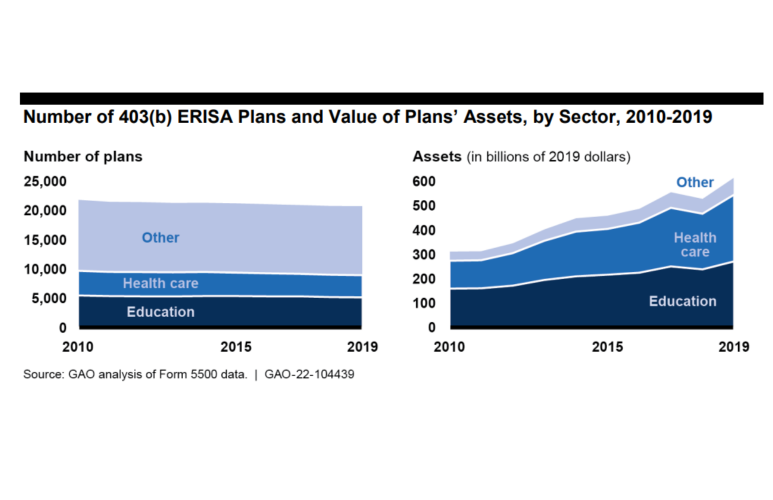

While 93% of the plans that held these assets are governed under the Employee Retirement Income Security Act of 1974 (ERISA), the value of the assets held by ERISA plans is considerably smaller. As of 2019, the latest year for which data is available, ERISA plan share value was $617 billion. Still, this represented significant growth from the $313 billion they held in 2010.

During the same period, non-ERISA plan assets fell from $538 billion to $469 billion, according to the report, Defined Contribution Plans: 403(b) Investment Options, Fees, and Other Characteristics Varied from the United States Government Accountability Office. The report was created to give background information on nonprofit retirement account activity to the U.S. House of Representatives Committee on Education and Labor.

Individual participation in ERISA plans reflected the total asset growth. The number of participants increased from 7.1 million in 2010 to 9.9 million in 2020.

What didn’t increase is the number of plans, which dipped from 21,900 to 20,900 between 2010 and 2019. Most individual ERISA plan participants come from either the healthcare (56%) or education (27%) sectors. “Significant merger and acquisition activity” within these sectors was a potential factor in the decline in the number of plans, according to the GAO report authors.

In contrast, 401(k) plans (commercial company-sponsored retirement accounts) realized a 17% increase in the number of plans and a 27% jump in the number of participants between 2010 and 2019. Asset levels within these plans jumped by 72%, aided by the fact that 401(k) plans can take advantage of investment opportunities not available to 403(b) plan participants, such as being able to purchase individual stocks.

Directional data indicates that in 2020 nonprofit and tax-exempt employers contributed an average of 4.6% of annual payroll to 403(b) accounts while participants contributed 6.2% of annual earnings. Both of those figures represent drops from 2019, when employers contributed 6.3% and participants put aside 7.2% of their annual earnings. The report authors cautioned that these percentages are estimates, and that comprehensive data on contribution rates does not exist.

The report authors cited research indicating 403(b) plans have an average of between 23 and 31 investment options available to participants between 2011 and 2020, while 401(k) plans offered an average of between 18 and 20 options. Report authors noted that some plan sponsors have reduced the number of investment options, partly in an effort to lower administrative fees.

Participation in these plans is by no means universal. According to the report authors’ calculations, among 403(b) employers 42.5% did not make a contribution to their employees plans, and 13.5% of employees did not make a contribution. Among 401(k) participants, 22.7% of employers did not make any contributions to these plans, and 10.8% of employees did not.

Report authors also asked 26 plan sponsors to indicate the impact of the coronavirus pandemic on 403(b) plan participants. Eight of the 26 reported an increase in hardship withdrawals while 18 indicated either that there had not been a change or they did not know.

The full report is available here: https://www.gao.gov/assets/gao-22-104439.pdf