Associations, labor unions, and social welfare organizations – those that don’t primarily receive tax-deductible contributions — will be among the organizations that will no longer have to file Schedule B, disclosing names and addresses of major donors to the Internal Revenue Service (IRS). The revised reporting requirements will take effect for the year ending December 2018, with returns generally filed May 15, 2019.

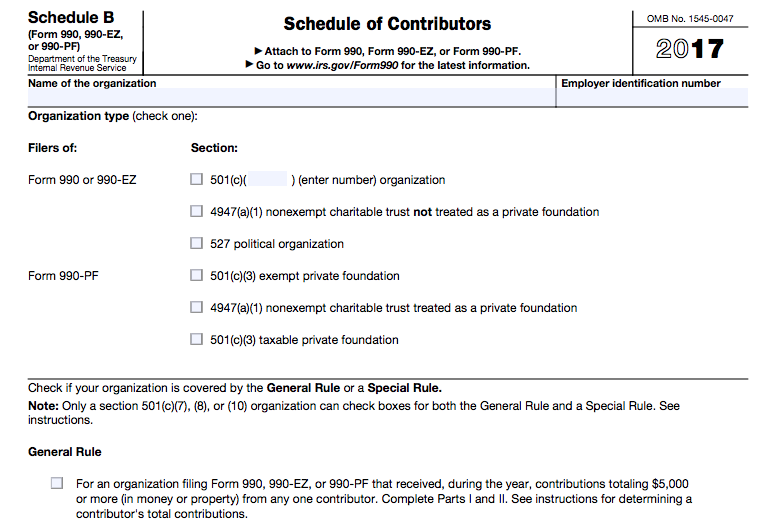

The U.S. Department of Treasury and IRS issued the announcement yesterday. Schedule B is part of the annual Form 990, disclosing names and addresses of substantial donors, generally considered $5,000 or more. Organizations would file the schedule with the IRS but only a redacted version, without names and addresses, would be public.

The 501(c)(3) charities and Section 527 organizations would still required to file Schedule B. The policy allows the IRS to confirm tax-deductible contributions by individuals.

Organizations would still have to collect and keep the information in their records and make it available to the IRS upon request, when needed to tax administration. If the information is needed for the purposes of an examination, the IRS will be able to ask the organization for it directly though it rarely audits tax-exempt organizations.

Treasury officials said the policy will avoid needless paperwork for both the organization and government and also reduce the risk of inadvertent disclosure or misuse of confidential information.

“This was never the intent of Congress to require such disclosure by all nonprofits,” said Cleta Mitchell, a partner at Foley & Lardner, LLP in Washington, D.C. “It serves no public policy imperative as the schedule is not public and, by law, confidential,” she said, adding that there have been disclosures by the IRS, which also has not explained its necessity for tax administration.

The issue of Schedule B filing and disclosure has become a great concern to conservative groups, Mitchell said, and one which has spawned lobbying efforts to get Congress to repeal the requirement for reporting donor information to the IRS.

Groups like Citizens United Foundation, Americans For Prosperity Foundation and Center for Competitive Politics have pushed back against Schedule B filing requirements enforced by attorneys’ general offices in New York and California. Mitchell argued that the state AGs were aiming to use donor information to chill donor contributions to conservative groups.

“The ruling is a strong signal that the IRS is backing away from active enforcement of the tax law applicable to tax-exempt organizations,” said Marcus Owens, who ran the Exempt Organizations Division of the IRS for a decade and now is a partner at Washington, D.C.-based Loeb & Loeb, LLP.

Mitchell called it “a great day for protecting speech in America,” applauding the Treasury Department and urging Congress to “finish the job by repealing the statutory requirement for 501(c)(3) organizations.”

A bill (H.R. 5053) to eliminate the Schedule B requirement was passed two years ago by the U.S. House of Representatives along a virtually party-line vote (240-182) but ultimately never got out of the Senate Finance Committee. Congressman Peter Roskam (R-Ill.) introduced the measure again (H.R. 4916) in this Congressional session, with 24 Republican co-sponsors, where it’s been in the Ways and Means Committee since February.

Others are wary that the policy change will open the door to more political activity by nonprofits and less transparency.

“It is a sad, unfortunate move, but one that been long in coming,” said Philip Hackney, an associate professor at the University of Pittsburgh Law School who also spent five years in the IRS Office of Chief Counsel. Schedule B was created in 1998 to try to avert disclosure problems but the information still occasionally improperly was made public, according to Hackney.

The requirement for charitable organizations is key to oversight from a tax-exemption perspective and is legislatively required. The elimination to other classes of nonprofits “does harm to our democracy and harm to the IRS’s ability to oversee the tax law generally,” he said. While he conceded the IRS has the authority to take the action and understands the reasons from an administrative perspective, Hackney said the IRS is willingly giving up important data points on where money is flowing in a tax-exempt manner from wealthy individuals, which will harm tax oversight. “It makes it more possible for wealth interests to influence our political system covertly,” he said.

Sen. Ron Wyden (D-Ore.), ranking member of the Senate Finance Committee, already has stated that he would oppose the nomination of Charles Rettig as IRS commissioner “unless he commits to restoring this critical IRS disclosure requirement.”

This is why I’ll be opposing Charles Rettig, nominee to be IRS Commissioner unless he commits to restoring this critical IRS disclosure requirement.

— Ron Wyden (@RonWyden) July 17, 2018

“The great concern is the combination of an effort to prevent the IRS to make it harder to find who’s funding whom. The (c)(4) political work made dark money darker,” said David Thompson, vice president of public policy at the National Council of Nonprofits. “It just made it a lot easier now for people to be heavily political in the nonprofit space” among social welfare organizations, labor unions and business leagues and associations.

“You can’t divorce this from the effort to weaken the Johnson Amendment,” he said, referring to the measure that bars 501(c)(3) charities from endorsing political candidates and electioneering.

“This new ruling is fuzzying more what 501(c)(4)s can and can’t do,” Thompson said. “It’s harder for the IRS to track down bad actors. To the extent it taints anything with the word nonprofit, we’re concerned,” he said, emphasizing that the new policy doesn’t change the rules for charitable nonprofits.

“If this means the IRS has to spend less time putting Schedule Bs in filing cabinets and gives them more time to enforce the law in support of charitable nonprofits, great. If it reduces the cost for the IRS to spend more money on important work, good,” said Thompson. Charities need regulatory guidance and needs the IRS to focus on weeding out bad actors in the sector, he added.

The complete seven-page Revenue Procedure 2018-38 is available here.